Covered Calls: Aligning Adjustments with Trade Benchmarks

Practical rules for rolling, holding, or accepting assignment of covered calls using delta, DTE and profit benchmarks.

Covered calls are a way to generate income by selling call options on stocks you already own. The trade-off? You collect a premium but cap your potential upside if the stock price rises above the strike. Managing these positions, especially when prices move unexpectedly, requires clear benchmarks to avoid emotional decisions.

Key dynamic exit strategies for adjustments include:

- Rolling out: Extend expiration for more income when the stock stays near the strike.

- Rolling up-and-out: Raise the strike and extend expiration to capture more upside during a rally.

- Rolling down: Lower the strike to collect fresh premium when the stock drops.

- Accepting assignment: Let the stock be sold at the strike, locking in profits.

Setting rules like delta thresholds, days to expiration (DTE), or minimum net credits ensures consistent decision-making. Tools like ThetaEdge help track performance across trades, providing metrics to refine strategies and meet income goals. The right adjustment depends on market conditions and your portfolio objectives.

1. Roll Strategies (Out, Up, Down)

Rolling a covered call involves closing your current short call and opening a new one with a different strike price, expiration, or both. Each type of roll is suited to specific market conditions.

Rolling out keeps the same strike price but extends the expiration date. This move is straightforward and focuses on generating additional income from time decay (theta). It’s a practical adjustment when the stock is moving sideways or hovering slightly above your strike price with plenty of time left before expiration.

Rolling up raises the strike price while keeping the same expiration date. This strategy is useful when the stock rallies, allowing you to capture some upside. However, it often requires a small debit, which reduces immediate income but expands your potential profit ceiling. The roll up-and-out combines both strategies - raising the strike price and extending the expiration. It’s a common tactic when a stock surges past your strike price. The additional time value often results in a net credit while increasing your maximum profit potential. For example, in April 2026, an investor holding 200 shares of AAPL (cost basis $192) had sold May 16 $200 calls for $3.50. When AAPL climbed to $211 by April 28, the calls were worth $12.40. The investor repurchased them and sold two June 20 $210 calls for $13.50, securing a $1.10 per share net credit ($220 total) while raising the profit cap by $10 per share ($2,000 additional potential profit). This approach highlights how adjusting based on benchmarks can help manage volatile markets.

Rolling down lowers the strike price while keeping the same expiration date. This defensive move is useful during a pullback, as it collects additional premium at the cost of a reduced profit ceiling. It’s a rule-based adjustment to maintain discipline during market declines. For instance, in May 2026, a trader holding a Salesforce (CRM) $265 call with 14 days to expiration bought it back for $0.90 and sold a $250 call for $2.67. This generated a $1.75 per contract net credit and boosted the annualized return potential from 8.2% to 24.5%.

Here’s a quick breakdown of how each roll type aligns with market conditions and its impact:

| Roll Type | When to Use | Impact on Total Return | Impact on Income |

|---|---|---|---|

| Roll Out | Sideways/stable stock | Unchanged | Increases (more theta) |

| Roll Up | Stock rallies moderately | Increases (higher cap) | Decreases (may cost debit) |

| Roll Down | Stock pulls back | Decreases (lower cap) | Increases (fresh premium) |

| Roll Up-and-Out | Sharp rally past strike | Increases (higher cap) | Increases (net credit) |

It’s important to avoid rolls that result in more than a $0.10 net debit. If the numbers don’t add up, it’s often better to allow assignment and start fresh rather than forcing a trade that no longer aligns with your original strategy. As Mustafa Bilgic from CoveredCallCalculator.net advises:

"A roll that does not produce a meaningful net credit is usually not worth the operational complexity."

Next, we’ll examine the hold-to-expiration approach and assignment strategies to refine your decision-making process further. You can also use portfolio intelligence tools to monitor these benchmarks automatically.

sbb-itb-a9ac3c2

2. Hold to Expiration and Assignment

When you hold a covered call through expiration, you can capture the entire initial premium if the option expires worthless. If the stock price ends above your strike price, assignment results in the maximum profit the trade was meant to achieve. This includes the difference between your cost basis and the strike price, plus the full premium you collected.

For example, a covered call yielding 2% in 30 days equates to a 24% annualized return. This can often outperform the risk-adjusted return of rolling the trade forward. If the stock gets assigned at your original exit target, it’s not a loss of shares but rather the successful execution of your strategy.

However, holding to expiration isn’t without its pitfalls. The biggest concern is gamma risk, particularly in the final week. A small 1% move in the stock price during this time can wipe out 10–20% of the remaining profit. As Tradetus explains:

"Beginners hold every covered call to expiration 'to capture every penny of premium.' This squeezes the last 10-20% of premium at the cost of much higher gamma risk in the final week."

Another challenge is pin risk, which arises when the stock closes exactly at your strike price on expiration day. This creates uncertainty about whether your shares will be assigned. To avoid unexpected after-hours assignments, it’s wise to close any in-the-money or at-the-money positions before 3:00 PM ET on expiration day.

To manage these risks, strategies like the 21-DTE rule and the 50% profit rule can be helpful. Closing or rolling the position 21 days before expiration captures most of the premium (theta) while steering clear of the volatile final days. Similarly, closing the trade once the short call has lost 50% of its value locks in profits efficiently and frees up capital for other opportunities. The table below outlines how these approaches compare:

| Strategy | Risk Profile | Income Consistency | Best Use Case |

|---|---|---|---|

| Hold to Expiration | High Gamma/Pin Risk | Variable | Flat stock; planned exit at strike |

| Close at 50% Profit | Minimal | High | Any market; focus on capital efficiency |

| Roll at 21 DTE | Low Gamma Risk | High | Trending or volatile markets |

| Accept Assignment | Minimal (trade ends) | N/A | Strike above cost basis; capital recycling |

Beyond risk reduction, assignment offers another advantage: it simplifies tax reporting. Instead of dealing with a series of rolling trades that might trigger wash sale rules, assignment results in a single taxable event - a capital gain or loss on the shares, plus the premium income .

3. ThetaEdge for Benchmark-Driven Adjustments

When refining your covered call strategies, having a structured analytics platform can make all the difference. Once you've chosen your adjustment method, it's crucial to measure its effectiveness against clear benchmarks.

ThetaEdge was designed to tackle this exact need. Instead of analyzing each covered call trade in isolation, it assigns a unique ID to every roll chain, providing complete visibility into the full lifecycle P&L for each trade .

The platform employs ledger-based accounting, keeping an immutable record of every premium collected, every closing trade, and every assignment. This approach eliminates the errors that often come with manual tracking, especially over multiple rolls. As CoverEdge explains:

"When shares get called away, your cost basis needs to account for ALL premiums collected across the entire chain - not just the last trade." - CoverEdge

To maintain consistency in income, ThetaEdge offers live metrics like annualized yield, breakeven points, and assignment P&L for each trade. These tools allow you to fine-tune your strategy based on post-trade benchmarks. Additionally, the platform tracks Portfolio Theta - the total daily income from time decay across all positions - helping you evaluate whether your portfolio is meeting its monthly income goals. For instance, in a $100,000 portfolio, a professional-grade theta target typically ranges between $50 and $200 per day.

Risk management is another key feature. ThetaEdge monitors metrics such as net delta (ideal range: 60–80%), sector concentration (alerts if above 40%), and cash reserves (recommended range: 15–25%). As expiration nears, the platform's AI provides actionable recommendations - Let Assign, Let Expire, Roll, or Review - based on technical indicators and your cost basis.

"The key number is the net credit - the premium received minus the cost to close. You want this to be positive whenever possible." - CoverEdge

For added convenience, ThetaEdge integrates with over 80 brokerages through secure, read-only access via SnapTrade, eliminating the need for manual data entry. The service is available through ThetaEdge One at $999 annually (about $83.25 per month when billed yearly), and it includes a 30-day free trial with full access.

Pros and Cons of Each Adjustment Method

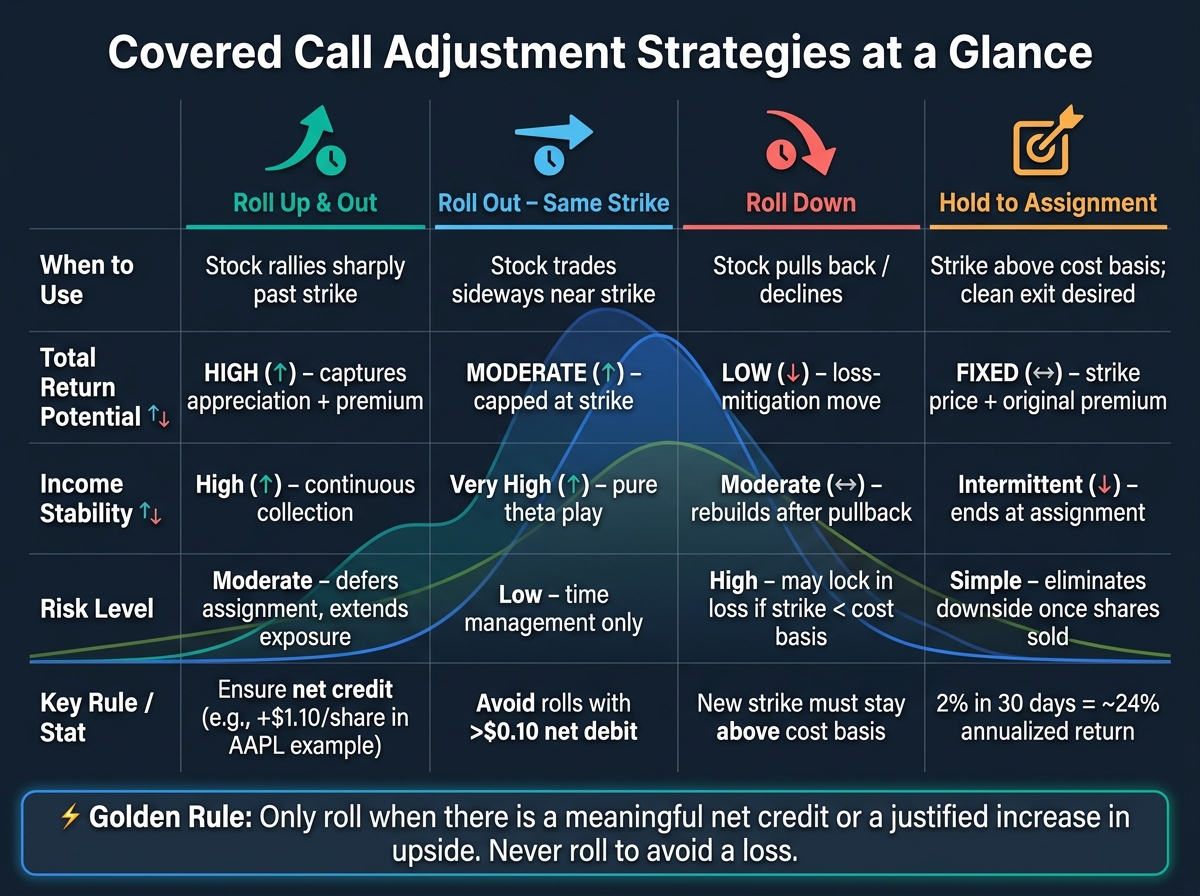

Covered Call Adjustment Strategies: A Visual Comparison Guide

Building on the covered call strategy basics, this section lays out the trade-offs for each adjustment method. No single approach works for every market condition. Each method involves balancing income potential, retained upside, and assumed risk. Knowing the strengths and weaknesses of each option allows you to make decisions based on logic and numbers rather than guesswork.

Rolling out (same strike, later date) is a straightforward move aimed at steady income. It focuses on collecting theta (time decay) without altering your profit cap, making it a good fit for stocks that are trading within a predictable range. However, it also means extending your exposure to the stock over time. Rolling up and out is more of a corrective measure, used when a stock rallies past your strike. It raises your profit ceiling and delays assignment, often for a small net credit. However, it requires you to maintain stock exposure and actively manage the position. Rolling down is a way to rebuild income by collecting fresh premium, but it comes with the risk of locking in a loss if the strike falls below your cost basis.

Holding to assignment is often underappreciated. As David Romic, a retail options trader, explains:

"Assignment is success, not failure. You collected premium on the way down (put), collected premium on the way up (call), and captured stock appreciation. Mission accomplished." - David Romic, Retail Options Trader

This method provides a clean exit. While income stops, so does the associated risk, freeing up your capital for new opportunities.

Here’s a quick comparison of how these methods affect returns, income, and risk:

| Method | Total Return Potential | Income Stability | Risk Management |

|---|---|---|---|

| Roll Up & Out | High - captures appreciation + premium | High - continuous collection | Moderate - defers assignment but extends exposure |

| Roll Out (Same Strike) | Moderate - capped at strike | Very High - pure theta play | Low - time management only |

| Roll Down | Low - often a loss-mitigation move | Moderate - rebuilds after pullback | High - lowers breakeven |

| Hold to Assignment | Fixed - strike price + original premium | Intermittent - ends at assignment | Simple - eliminates downside once shares are sold |

When deciding to roll, ensure that either a net credit or a meaningful upside justifies the additional exposure. Avoid rolling into expirations that overlap with earnings announcements unless you're prepared for the increased volatility. While these moves can sometimes appear attractive on paper, they often carry hidden risks. These guidelines help refine your approach, ensuring your adjustments align with your broader trading objectives.

Conclusion

Managing covered calls effectively boils down to one fundamental principle: stick to predefined benchmarks rather than letting emotions dictate your decisions. The benchmarks discussed in this article aim to create a structured, repeatable framework for making adjustments, ensuring that every move aligns with a well-thought-out strategy.

Using predefined rolling rules consistently outperforms making decisions on the fly. This isn't about picking the perfect stock - it's about sticking to a plan. Knowing exactly how you'll respond when a position moves against you, and acting decisively, is what sets disciplined investors apart.

"The investors who quietly compound through every market... are the ones who know the four covered call adjustment strategies cold and pull the trigger without flinching." - CashFlowMachine

Your choice of adjustment method depends on your overall objective. For steady income, rolling out at the same strike is often the go-to move. If the stock surges, rolling up and out allows you to capture more upside while still collecting premium. When a stock drops, rolling down can rebuild income - but only if the new strike remains above your cost basis. And when the math doesn’t justify a roll, accepting assignment can often be the smartest play. Staying clear on these strategies reinforces the discipline needed for successful covered call management.

FAQs

When should I roll versus accept assignment?

Stick to your original investment goals when making your decision. If the strike price matches your target sale price or if the stock’s fundamentals have shifted, making it less appealing, accepting assignment might make sense.

If you remain optimistic about the stock’s future, consider rolling the option. This approach works if you’re looking to capture more potential upside or continue generating income. Focus on rolling for a net credit - if it requires a debit, take a step back and re-evaluate the trade. Avoid rolling simply to postpone an exit or due to emotional attachment to the position.

What benchmarks (delta, DTE, profit %) should I use to manage covered calls?

To handle covered calls effectively, many traders stick to specific benchmarks for timing and profit goals. Opening positions typically works best with 30-45 days to expiration (DTE), while adjustments are often made at 21 DTE or after achieving 50% profit. When selecting strike prices, a 0.20-0.30 delta provides a more cautious approach, while 0.50+ deltas aim for higher income but come with increased risk. Rolling positions is commonly considered when the delta reaches 0.60-0.70. Tools like ThetaEdge can help tailor these benchmarks to fit the unique needs of your portfolio.

How do I track my true cost basis across multiple rolls?

Tracking your true cost basis through multiple rolls means accounting for every transaction in the roll chain. Net credits reduce your cost basis, while net debits push it higher. As rolls become more intricate, manually keeping tabs can lead to mistakes. That’s where ThetaEdge steps in - it automatically tallies all credits and debits, presenting a clear break-even point. Plus, it provides portfolio-aware insights, helping you make smarter adjustments with ease.