Protective Puts: Basics for Self-Directed Investors

Learn how protective puts cap stock losses, the premium trade-offs, choosing strike and expiration, and when to hedge concentrated or volatile positions.

Protective puts are a straightforward way to manage risk in your investment portfolio. By purchasing a put option for stocks you own, you gain the right to sell your shares at a set price, no matter how much the market drops. This strategy acts as a safety net, limiting potential losses while allowing you to benefit from stock gains, minus the cost of the put.

Here’s why investors use protective puts:

- Risk Management: Protects against sharp declines in stock price.

- Flexibility: Keeps your shares intact while providing downside protection.

- Tax Efficiency: Avoids triggering capital gains taxes compared to selling.

- Volatility Buffer: Useful during earnings reports or regulatory changes.

The trade-offs? Protective puts require an upfront premium, which can eat into returns if the stock price stays flat or rises. Selecting the right strike price and expiration date is key to balancing cost and protection.

For example, if you own 100 shares of a stock at $62 and buy a $60 strike put, you’re protected from losses beyond $2 per share. If the stock falls to $50, the put offsets most of the loss. However, if the stock rises, the put expires worthless, and you lose only the premium paid.

Protective puts are particularly helpful for concentrated stock positions or when markets are unpredictable. While they aren’t free, the peace of mind they provide during uncertain times can make them a valuable tool in your risk management arsenal.

How Protective Puts Work

The Mechanics Behind Protective Puts

A protective put works like a safety net for your stock holdings. If the stock price drops below the strike price of your put option, the value of the option increases, helping to offset your losses. Here’s a simple example: imagine you own 100 shares of a stock trading at $62. If the stock falls to $50, you’d typically face a $1,200 loss. However, if you’ve purchased a protective put with a $60 strike price, the put option gains $10 per share (totaling $1,000), significantly reducing your overall loss.

"The strike price of the put option acts as a barrier where losses in the underlying stock stop." - Investopedia

If the stock price rises, the put option expires worthless, but you still benefit from the stock’s gains, minus the premium you paid for the put. On the other hand, if the stock price stays flat, the put loses value over time due to time decay (theta), which accelerates as the option nears expiration.

Let’s take a closer look at how strike price, expiration, and breakeven points influence this strategy.

Strike Price, Expiration, and Breakeven

Selecting the right strike price involves balancing risk and reward to find the right mix of cost and protection. For instance:

- At-the-money (ATM) puts, where the strike equals the current stock price, provide complete protection but come with a higher premium.

- Out-of-the-money (OTM) puts, with a strike below the current stock price, cost less but act like a deductible, covering losses only after an initial drop. For example, if your stock trades at $62 and you buy a $60 strike put, you’re agreeing to absorb the first $2 of loss per share.

Expiration timing also plays a key role. Longer-term puts cost more but provide extended coverage, while shorter-term options (30–60 days) strike a balance between affordability and practicality.

Your breakeven point is straightforward to calculate: add the premium you paid to the stock’s purchase price. For example, if you bought shares at $62 and paid a $1 premium ($100 for 100 shares), your breakeven would be $63. The stock must rise above this level for your position to turn profitable.

| Strike Price Type | Premium Cost | Protection Level | Best For |

|---|---|---|---|

| At-the-Money (ATM) | High | Maximum (100% floor) | High-risk events like earnings |

| Out-of-the-Money (OTM) | Low to Moderate | Partial (floor below market) | General hedging with lower costs |

sbb-itb-a9ac3c2

Risk and Reward of Protective Puts

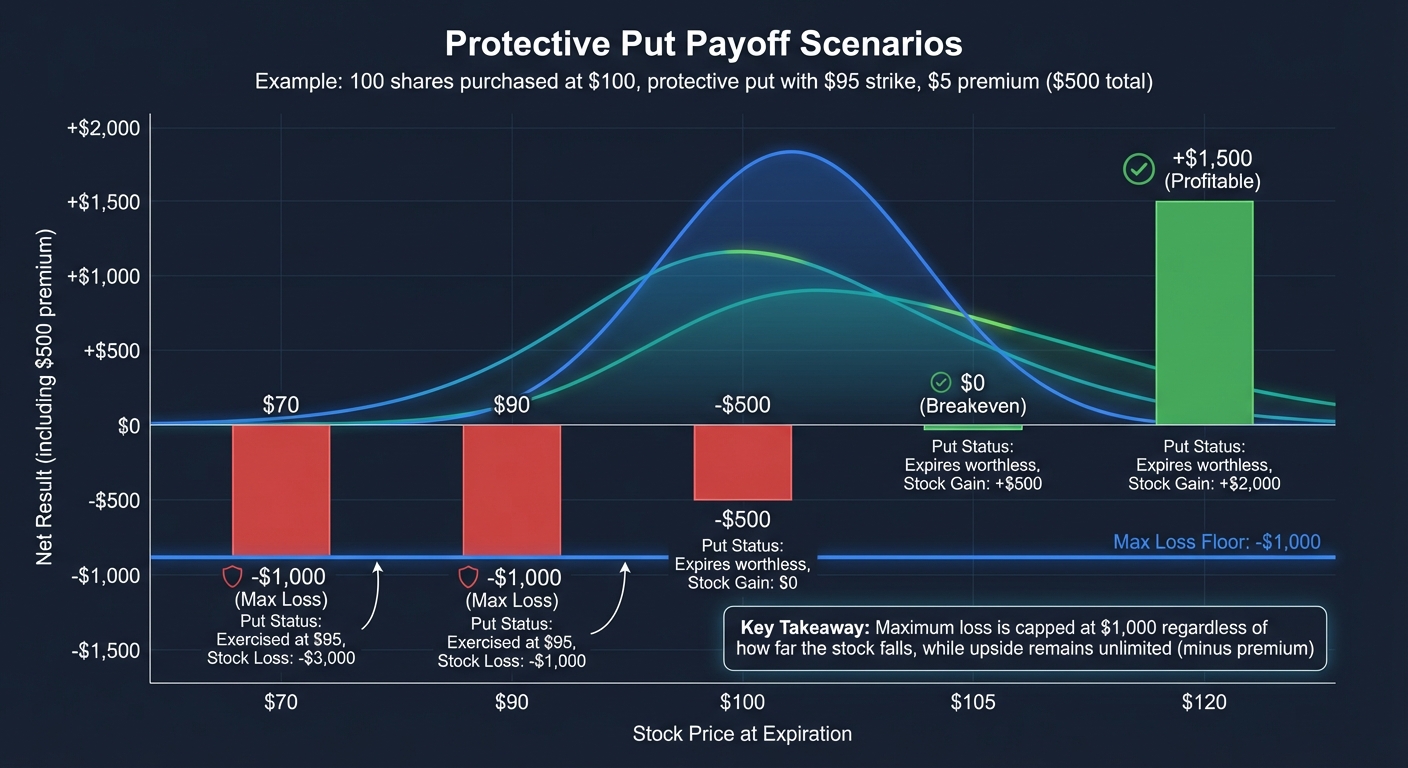

Protective Put Payoff Scenarios: Stock Price Impact on Returns

Understanding Payoff Scenarios

A protective put offers what traders describe as an asymmetric payoff - your potential losses are limited, while your gains remain open-ended (minus the premium you paid).

Here’s how it works: your maximum loss is confined to the difference between your stock’s purchase price and the put’s strike price, plus the premium. For example, if you bought shares at $100 and purchased a $95 strike put for $5 per share, the most you could lose is $10 per share, no matter how far the stock drops. Without that put, a drop to $70 would leave you with a $30 per share loss.

The table below breaks down how different stock prices at expiration affect your position:

| Stock Price at Expiration | Put Option Outcome | Stock Gain/Loss | Net Result (including $500 premium) |

|---|---|---|---|

| $120 | Expires worthless | +$2,000 | +$1,500 |

| $105 | Expires worthless | +$500 | $0 (Breakeven) |

| $100 | Expires worthless | $0 | -$500 |

| $90 | Exercised at $95 | -$1,000 | -$1,000 (Max Loss) |

| $70 | Exercised at $95 | -$3,000 | -$1,000 (Max Loss) |

With this risk-reward profile in mind, it’s essential to consider how the cost of the premium impacts your returns.

The Cost of Protection

While protective puts limit losses, they come at a price. The premium you pay for this protection directly eats into your returns in markets that remain stable or rise. Much like car insurance, you pay the cost regardless of whether you end up using it. This means your stock must gain enough to cover the premium before you see any real profit. For instance, if you spend 3% of your position’s value on protective puts each quarter, your stock needs to appreciate by more than 12% annually to offset this expense.

The costs can add up quickly, especially for high-volatility stocks. Take Tesla (TSLA) as an example: an investor holding 100 shares at a $300 cost basis, with the stock trading at $430.90, could purchase a 430-strike put for $28.00, or $2,800 total. A 2-year put would cost 25.6% of the position’s value, while rolling 23-day puts annually would skyrocket costs to 74%. This shows how frequent hedging can significantly erode returns.

For this reason, most individual investors use protective puts strategically rather than relying on them as a permanent feature of their portfolios. They might employ them for concentrated positions, ahead of major events like earnings announcements, or during periods of heightened market uncertainty. The challenge lies in finding the right balance between the reassurance of downside protection and the drag that premiums can place on returns in calmer markets.

When to Use Protective Puts

Protecting Concentrated Stock Positions

Protective puts are particularly useful when a large portion of your portfolio is tied up in a single stock, and selling isn’t a practical option. This situation often arises with employer-restricted stock, inherited shares with a low tax basis, or stocks with significant unrealized gains that could lead to hefty capital gains taxes if sold. By purchasing a put, you lock in a fixed exit price, providing a safety net against losses while deferring any taxable events.

Navigating Market Volatility

Market-moving events - such as earnings reports, regulatory decisions, or major product launches - can lead to sharp, overnight price changes. Protective puts are a powerful tool in these scenarios because they guarantee an exit price, unlike stop-loss orders, which may execute at unfavorable levels during volatile gaps.

Take the case of Celladon Corporation (CLDN) in April 2015. On Friday, April 24, the stock closed at $13.68. Over the weekend, negative news emerged, and by Monday morning, the stock opened at just $2.93. Investors relying on a $10 stop-loss order saw their shares sold at $2.93, far below their intended exit price. However, those holding a protective put with a $10 strike price avoided this scenario, selling their shares at the predetermined level and significantly limiting their losses.

Protective Puts vs. Stop-Loss Orders

The choice between protective puts and stop-loss orders often boils down to cost versus certainty. Stop-loss orders are free to set up but convert to market orders when triggered, which can lead to execution at much lower prices during volatile conditions. Protective puts, on the other hand, require an upfront premium but provide absolute certainty - you can sell at the strike price regardless of how far or how quickly the stock drops.

| Feature | Protective Put | Stop-Loss Order |

|---|---|---|

| Upfront Cost | Premium required | Generally free |

| Exit Price | Guaranteed at strike price | Not guaranteed; subject to slippage |

| Position Status | Retain ownership of shares | Position is sold/closed |

| Market Gaps | Fully protected against gaps | Vulnerable to opening gaps |

Another important advantage of protective puts is that they allow you to keep your position intact. If the stock rebounds after a brief dip, you can still benefit from the recovery. Stop-loss orders, by contrast, close your position entirely, which could leave you sidelined if the stock quickly recovers after triggering the order.

Using ThetaEdge for Protective Put Analysis

Portfolio-Specific Analysis

ThetaEdge connects to your brokerage account in read-only mode, making it easy to analyze your portfolio automatically. With compatibility across more than 80 brokerages, the option intelligence platform has reviewed millions of dollars in assets to identify concentration risks. For instance, it flagged a 25.3% position in AAPL as "High Risk" because it exceeded recommended single-position limits. These flagged positions often serve as ideal candidates for protective puts. ThetaEdge then provides pre-assessed strategies, outlining key details such as strike prices, expiration dates, premium costs, assignment probabilities, and breakeven points. Beyond this, the platform uses AI to deliver even deeper insights into your portfolio's risks.

AI-Powered Portfolio Insights

With Thetix AI, you can ask plain-English questions tailored to your portfolio and receive actionable answers based on live market data and your holdings. For example, you could ask, "What is the risk on my AAPL position?" and instantly receive a detailed downside analysis. The AI can also compare implied volatility across holdings - like AMD's 54.9% versus NVIDIA's 42.2% - to highlight differences in protection costs. Additionally, Thetix generates statistical price forecasts, covering Bear Case (-1σ), Base Case, and Bull Case (+1σ) scenarios, helping you with strike price selection for your strategy.

"It feels like having a market analyst on call. I ask a question, Thetix gives me an answer I can understand and use right away."

- Jordan E., IT Architect

You can save your most-used analyses as Thetix Cards, which update automatically, and set Thetix Alerts to notify you of specific conditions - like volatility spikes - that may signal the need for protection. These tools integrate seamlessly with ThetaEdge's brokerage connection, making it easier to align insights with your overall strategy.

Brokerage Integration

ThetaEdge's read-only integration uses your actual cost basis and position sizing to deliver personalized analysis, while leaving all trading decisions in your hands. By syncing live cost basis and position data, the platform ensures that any protective put strategies are tailored precisely to your portfolio's risk profile.

"I keep my accounts where they are, and everything's explained in plain language. It's been way easier than I thought."

- Sarah C., Marketing Director

ThetaEdge is free to try, offering a 30-day full trial that includes features like protective put analysis, concentration risk identification, and AI-powered insights. Acting purely as an analytical tool - not a trading bot or advisor - it gives you full control over your investment decisions.

Conclusion

Protective puts offer individual investors a reliable way to manage risk, functioning like an insurance policy for your portfolio. They establish a guaranteed floor price for your holdings while still allowing for upside potential. Unlike stop-loss orders, which depend on market execution, a protective put ensures the right to sell at the strike price, providing a more secure option for managing concentrated positions, handling earnings-related volatility, or safeguarding unrealized gains without triggering immediate capital gains taxes.

Executing this strategy effectively requires careful consideration of strike price selection, expiration timing, and premium costs, which typically range from 1%–3% of portfolio value annually. Timing is crucial - buying protection during periods of low implied volatility can help keep premiums manageable. For ongoing coverage, rolling 30- to 45-day puts is a common approach, as it maintains protection while preserving time value.

For those looking to simplify the process, tools like ThetaEdge can be invaluable. This platform connects to your brokerage in read-only mode, identifies concentration risks, and suggests tailored protective put strategies. It provides detailed recommendations, including strike prices, expiration dates, premium costs, and breakeven points. Its AI feature allows you to ask portfolio-specific questions in plain English, such as comparing volatility across assets or evaluating downside risks, delivering actionable insights based on your actual holdings and live market data.

As TradeStation aptly puts it:

"The protective put strategy effectively serves a remarkably similar purpose [to homeowner's insurance] - they act as an insurance policy for your stock positions, providing peace of mind while allowing you to participate in potential upside gains."

- TradeStation

ThetaEdge enhances this approach with its free 30-day trial, offering thorough protective put analysis, risk identification, and AI-driven insights - all while leaving the final decisions in your hands.

FAQs

How do I choose the best put strike price?

When deciding on the ideal strike price for a protective put, it's all about finding a match between your comfort with risk and your outlook on the market. Some investors prefer a strike price close to the stock's current price, as this offers the highest level of protection. On the other hand, selecting a lower strike price can lower the premium cost, though it also means accepting a greater degree of risk. The real challenge lies in striking the right balance between how much you're willing to spend on the premium and the amount of downside risk you feel prepared to handle.

How far out should I buy the put expiration?

When navigating market fluctuations, securing protection through put options can be a wise move. Opt for expiration dates that are at least 3 to 6 months away, depending on your investment goals and how much risk you're comfortable taking on. While longer expirations offer greater flexibility, keep in mind that they typically come with higher premiums. Balancing cost and coverage is key to making this strategy work for you.

When is a protective put worth the premium?

A protective put becomes worthwhile when the cost of the option aligns with the potential loss it shields you from. This approach offers a safety net against downside risk, limiting losses on the underlying stock while still allowing you to keep ownership of your shares.