Covered Calls vs Cash-Secured Puts: Which Is Better?

Compare covered calls and cash-secured puts — requirements, income potential, risks, and when each strategy fits your portfolio and market outlook.

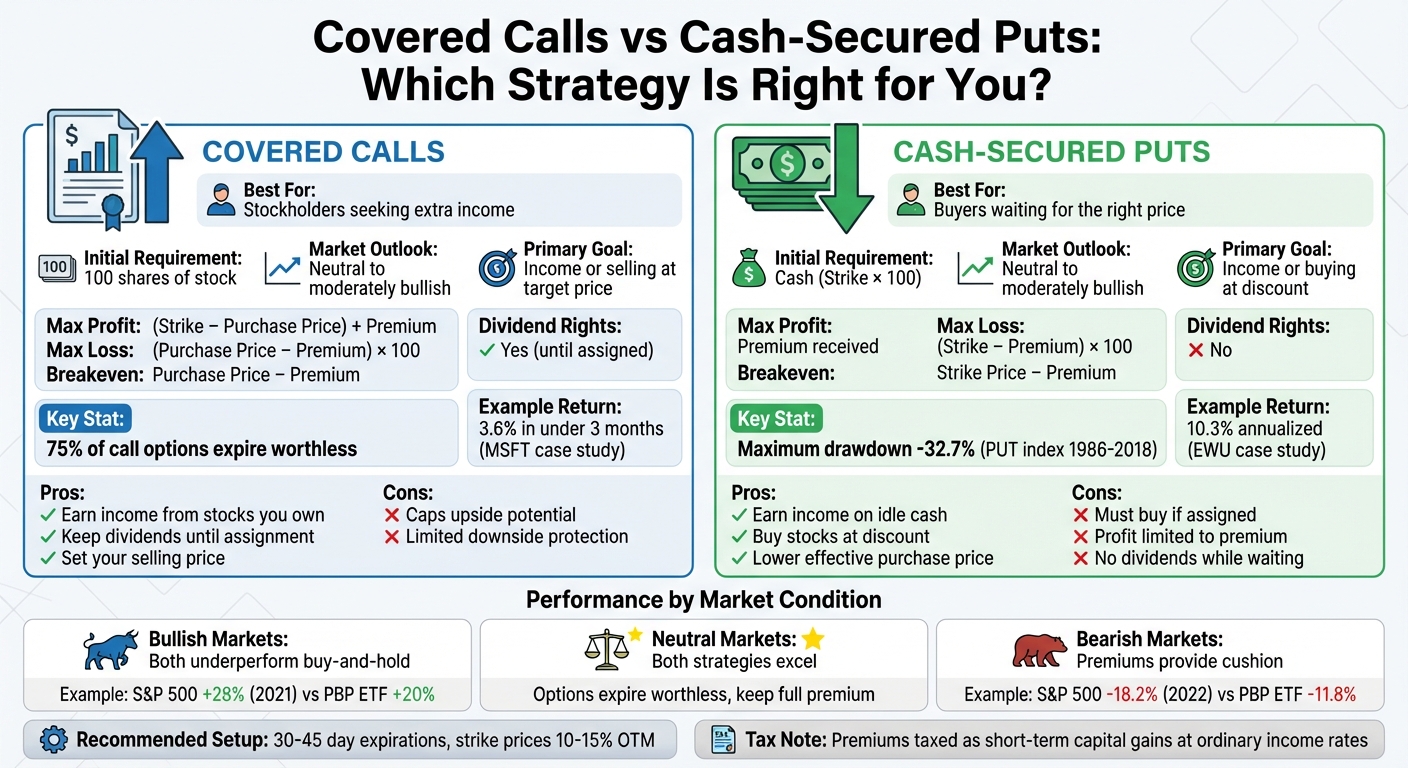

When deciding between covered calls and cash-secured puts, the choice depends on your current portfolio and investment goals. Both strategies generate income through premiums and work best in neutral to mildly bullish markets. Here's a quick breakdown:

- Covered Calls: Ideal if you already own 100 shares of a stock and want to earn income while potentially selling at a target price. You keep dividends until the stock is sold but cap your upside if the stock rises significantly.

- Cash-Secured Puts: Best if you have cash on hand and are looking to buy stock at a discount. You earn premiums while waiting, but you'll need to buy the stock if it drops below the strike price.

Both strategies carry risks if the stock price falls sharply. Covered calls suit those looking to generate income from stocks they own, while cash-secured puts are better for those wanting to acquire stocks at a lower cost.

Quick Comparison

| Factor | Covered Call | Cash-Secured Put |

|---|---|---|

| Initial Requirement | 100 shares of stock | Cash (Strike × 100) |

| Market Outlook | Neutral to mildly bullish | Neutral to mildly bullish |

| Max Profit | (Strike - Purchase Price) + Premium | Premium received |

| Max Loss | (Purchase Price - Premium) × 100 | (Strike - Premium) × 100 |

| Breakeven | Purchase Price - Premium | Strike Price - Premium |

| Dividend Rights | Yes (until assigned) | No |

| Primary Goal | Income or selling at a target price | Income or buying at a discount |

Covered calls work well for stockholders seeking extra income, while cash-secured puts are a solid choice for buyers waiting for the right price. Both strategies require careful risk management and align with different financial objectives.

Covered Calls vs Cash-Secured Puts: Side-by-Side Comparison

Should You Sell Covered Calls or Cash Secured Puts

How Covered Calls Work

A covered call strategy starts with owning 100 shares of a stock per contract. After acquiring the shares, you sell a call option, giving someone else the right to buy your stock at a specific strike price before the option expires. In return, you receive an upfront payment called a premium, which you keep no matter what happens.

This approach benefits from time decay, also known as Theta. As the expiration date approaches, the option’s time value decreases, which works in your favor. Interestingly, about 75% of all call options expire worthless, meaning you get to keep both the premium and your shares. For instance, in November 2022, an investor holding 100 Microsoft Corp. (MSFT) shares at $242 sold a call option with a $250 strike price, expiring in January 2023, for a $10 premium per share. By January 2023, MSFT closed at $240, rendering the option worthless. The investor kept the $1,000 premium and their shares. Even though the stock dropped by $2, the investor achieved a net gain of $8.68 per share (including a $0.68 dividend), translating to a 3.6% return in under three months.

Setting Up a Covered Call

There are two main ways to set up a covered call. You can use a "buy-write", where you buy shares and sell a call option simultaneously, or an "overwrite", where you sell a call option on shares you already own. Many investors aim for strike prices 10% to 15% above the current stock price, with contracts expiring in 30 to 45 days to balance premium income and potential capital gains.

Tools like ThetaEdge help investors analyze portfolios by offering risk/reward metrics and probabilities of assignment.

Maxim Khailo, the Founder & CEO of ThetaEdge, explains: "Running the hedge fund, I created institutional tools that could analyze thousands of scenarios in real-time... ThetaEdge empowers them to do it with the same tools the elite have always used".

These setup details play a big role in determining your income potential and managing risks.

Income and Risk Factors

The premium you earn provides immediate income and creates a buffer against losses. Your breakeven point becomes the stock’s purchase price minus the premium collected. However, this strategy comes with a trade-off: your potential profit is limited. If the stock price rises above your strike price, your shares will likely be "called away" (sold at the strike price), and you won’t benefit from any additional gains. Automatic exercise happens when the stock price exceeds the strike price by $0.01 at expiration.

While the premium can cushion losses, it doesn’t eliminate them entirely. If the stock’s price drops significantly, you’ll still face losses, offset only by the premium. To manage this risk, you can "roll" the position - buying back the current call and selling another with a later expiration or a higher strike price. Rolling positions helps maintain an income-focused approach. Additionally, avoid selling covered calls just before earnings announcements, as significant price swings could lead to unexpected assignments or missed opportunities for gains. managing risks like assignment and time decay is an essential part of evaluating whether covered calls align with your investment goals.

How Cash-Secured Puts Work

Cash-secured puts, like covered calls, generate income through premiums but differ in how they're executed and their risk profile. This strategy involves selling a put option while setting aside enough cash to potentially buy 100 shares of the underlying stock at the strike price. In return, you receive a premium upfront, which you keep regardless of the option's outcome. It's a go-to approach for investors who are neutral to moderately bullish, aiming to earn income on idle cash or buy stocks at a discount.

Here’s how it works: If the stock price stays above your strike price until the option expires, the put expires worthless, and you keep the premium as profit. On the other hand, if the stock price falls below the strike price, you’ll purchase 100 shares at an effective cost equal to the strike price minus the premium. This setup appeals to many investors because it offers two potential benefits: earning income if the option isn’t exercised or buying shares at a lower price if it is.

"You're essentially getting paid to wait for a better entry price", says Ryan Peterson, Contributor at Benzinga.

For instance, in February 2023, an investor considered the iShares MSCI United Kingdom ETF (EWU), trading at $32.62. By selling a July 21 put with a $32 strike price for a $1.25 premium, the investor could earn $125 per contract. If assigned, the effective purchase price would be $30.75 (strike price minus premium), representing a 5.8% discount from the market price. If the ETF stayed above $32, the premium would provide a 4.1% return on capital, or 10.3% annualized.

Setting Up a Cash-Secured Put

To implement this strategy, you’ll need to reserve cash equal to the strike price × 100. For example, a $50 strike price requires $5,000 in cash. This cash reserve is what sets cash-secured puts apart from riskier naked puts, which rely on margin and could lead to forced liquidations if the trade moves against you.

Tools like ThetaEdge can help you assess assignment probabilities and cash requirements, making it easier to spot income opportunities that align with your portfolio and available capital. Many investors favor out-of-the-money (OTM) strike prices with expirations of 30 to 45 days. This timeframe strikes a balance between earning premium income and managing the risk of assignment.

Income and Risk Factors

The premium you collect provides immediate income and lowers your effective purchase price if assigned. Your breakeven point becomes the strike price minus the premium. However, the trade has limits: your maximum profit is capped at the premium received. If the stock price drops significantly, you’ll still need to buy shares at the strike price, even if their market value is much lower.

Because of this, it’s wise to sell puts only on stocks you’re comfortable owning long-term. Keep a close eye on your positions as expiration nears. If the stock price rises significantly, you might want to buy back the put at a lower price, locking in profits and freeing up cash for other opportunities.

sbb-itb-a9ac3c2

Covered Calls vs. Cash-Secured Puts: Direct Comparison

Side-by-Side Comparison Table

Both covered calls and cash-secured puts are strategies designed to generate premiums in markets that are neutral to mildly bullish. However, their mechanics and requirements set them apart, influencing which one might fit better with your investment goals.

| Factor | Covered Call | Cash-Secured Put |

|---|---|---|

| Initial Requirement | 100 shares of stock | Cash (Strike × 100) |

| Market Outlook | Neutral to moderately bullish | Neutral to moderately bullish |

| Max Profit | (Strike - Purchase Price) + Premium | Premium received |

| Max Loss | (Purchase Price - Premium) × 100 | (Strike - Premium) × 100 |

| Breakeven | Purchase Price - Premium | Strike Price - Premium |

| Dividend Rights | Yes (until assigned) | No |

| Primary Goal | Income or exiting a position | Income or entering a position |

The capital needed for each strategy differs. Covered calls require owning at least 100 shares of the stock, which could mean a significant upfront investment. On the other hand, cash-secured puts demand cash equal to the strike price multiplied by 100. For example, a $50 strike price would require $5,000 in cash.

When it comes to maximum profit, covered calls offer potential gains from both the premium and stock appreciation up to the strike price. In contrast, cash-secured puts limit your profit to the premium received. On the downside, both strategies carry similar risks. If the stock's value plummets to zero, losses will be substantial, though the premium provides a slight offset.

An important distinction lies in dividend eligibility and option pricing. Covered call writers can still collect dividends as long as they own the shares and the option hasn’t been exercised before the ex-dividend date. Cash-secured put writers don’t receive dividends because they don’t yet own the stock. This difference can significantly impact returns, especially when dealing with dividend-paying stocks.

Performance Under Different Market Conditions

The success of these strategies heavily depends on market trends. In bullish markets, both strategies tend to underperform compared to simply holding the stock. Gains are capped - either at the strike price for covered calls or by the premium for cash-secured puts. For instance, in 2021, the S&P 500 surged over 28%, while the Invesco S&P 500 BuyWrite ETF (PBP), which employs a covered call strategy, delivered only a 20% return.

In neutral or flat markets, both strategies excel. Stock prices remaining steady often result in options expiring worthless, allowing you to keep the full premium and repeat the process. This scenario is ideal for generating consistent income.

In bearish markets, premiums offer some protection but don’t eliminate risk. For example, during 2022's bear market, the S&P 500 fell 18.2%, while the PBP ETF, benefiting from premiums, only declined by 11.8%. However, both strategies still expose you to significant losses if the stock price drops well below your breakeven point.

The risk profiles of the two strategies also differ slightly. Cash-secured puts often carry slightly lower risk because put strikes are typically set below the current market price, allowing you to "buy at a discount" if assigned. Covered calls, on the other hand, expose you to price declines starting from the current stock price since you already own the shares. This subtle difference can influence which strategy aligns better with your risk tolerance and portfolio goals.

Choosing the Right Strategy for Your Goals

When Covered Calls Work Best

Covered calls are a great way to generate extra income from stocks you already own, especially if you're not planning to sell them anytime soon. This strategy works well when you expect the stock to stay relatively stable or rise slightly. For long-term investors holding dividend-paying stocks, covered calls offer an additional income stream without needing to part with their shares.

"Covered calls are ideal for investors who already own stock and are looking to generate passive income... Cash-secured puts suit investors looking to buy stock at a discount, while earning premium income in the meantime." - Ryan Peterson, Contributor, Benzinga

This method is also handy if you have a specific price in mind for selling your shares. For instance, if you bought a stock at $45 and are willing to sell it at $50, you can write a covered call with a $50 strike price. While waiting, you collect the premium. If the stock hits $50, you sell at your target price and keep the premium. If it doesn’t, you still hold onto your shares and the premium. However, there’s a trade-off: covered calls limit your potential gains. If the stock soars to $60, you’ll miss out on those extra profits since your shares will be sold at the $50 strike price. This makes covered calls less suitable if you’re highly optimistic about a stock’s potential for significant gains.

If you’re sitting on cash instead of stock, though, you might want to consider a different strategy.

When Cash-Secured Puts Work Best

Cash-secured puts are a smart choice when you’re neutral to slightly bullish on a stock but think it’s currently overpriced. This strategy lets you earn income on unused cash while giving you the chance to buy shares at a lower price.

"A cash-secured put is an options strategy that can generate income and potentially help you buy stocks at a lower price." - Fidelity

Here’s how it works: selling a put with a $50 strike for a $2 premium means your breakeven price is $48. If the stock price drops and you’re assigned at $50, the premium reduces your effective cost. This approach is best for stocks you’d be happy to own long-term, as there’s always the risk of the stock falling significantly below the strike price. For context, between June 1986 and December 2018, the PUT index experienced a maximum drawdown of -32.7%, which was less severe than the S&P 500’s -50.9% during market downturns.

Both strategies require thoughtful analysis to maximize their benefits - and that’s where tools like ThetaEdge come in.

Using ThetaEdge to Make Better Decisions

ThetaEdge simplifies the decision-making process by providing tailored insights for both covered calls and cash-secured puts. It offers professional-grade metrics, like risk/reward ratios and assignment probabilities, to help align your strategy with your portfolio and market outlook.

The platform’s Thetix AI assistant delivers actionable suggestions based on your specific income targets, while daily AI-generated action plans highlight the best opportunities without requiring constant monitoring.

Additional features include an income tracking dashboard to measure performance, portfolio Greeks to assess overall exposure, and integration with over 80 brokerages, allowing you to manage all your positions in one place. These tools ensure you have the data and support needed to choose the strategy that best fits your goals.

Conclusion

Both covered calls and cash-secured puts are effective ways to generate income in markets that are neutral to moderately bullish, but they serve different purposes. Covered calls work best for investors who already own stock and want to earn extra income while setting a potential selling price. On the other hand, cash-secured puts are suited for investors with idle cash who wish to buy stock at a discount while earning premium income.

The choice between these strategies depends largely on what you currently hold and your outlook for the market. If you already own shares and expect only modest price changes, a covered call allows you to earn premiums without necessarily selling your stock - unless it hits your desired price. If you're sitting on cash and waiting for a more attractive entry point, a cash-secured put lets you collect premiums while potentially acquiring shares at a lower price if the stock falls below the strike.

It’s important to remember that both strategies carry risks, particularly if the stock price drops significantly. The premium you receive can offset some losses, but it won’t eliminate them. Timing your strategy to the market is crucial. For example, covered calls aren't ideal during highly bullish markets because they limit your upside potential. Similarly, cash-secured puts can lead to overpaying in bearish markets if prices continue to decline.

Lastly, keep taxes in mind. Premiums earned are generally taxed as short-term capital gains, which means they’re taxed at ordinary income rates. Using tax-advantaged accounts like IRAs can help preserve more of your earnings.

FAQs

What are the tax considerations for covered calls and cash-secured puts?

In the United States, taxes on covered calls and cash-secured puts depend on how each transaction unfolds.

For covered calls, the premium you earn when selling the call is generally treated as a short-term capital gain. If the option is exercised, meaning you sell the underlying stock, your total gain or loss will be calculated based on the stock’s holding period and cost basis. If the option expires without being exercised, the premium remains a short-term gain.

When it comes to cash-secured puts, the premium you receive is also classified as a capital gain. If the option is exercised and you end up buying the stock, the premium adjusts your cost basis for those shares. If the option expires unexercised, the premium is treated as a short-term gain.

Tax rules can be complex and subject to change, so it’s wise to consult a tax professional for personalized guidance.

How can I choose between covered calls and cash-secured puts for my investment strategy?

Choosing between covered calls and cash-secured puts comes down to your investment goals, market outlook, and comfort with risk.

If you already own a stock and expect it to stay flat or rise slightly, covered calls can be a solid way to earn extra income. By selling call options, you collect premiums while agreeing to sell the stock at a specific price if the option is exercised. This strategy also offers a small buffer against losses if the stock price drops, though it doesn’t eliminate risk entirely.

On the other hand, if there’s a stock you’re interested in buying and you think its price might dip or stay steady, cash-secured puts could be a better fit. With this approach, you sell put options, collect premiums upfront, and set aside cash to buy the stock at the strike price if the option is exercised. This strategy works well if you’re comfortable owning the stock at that price.

In short, use covered calls to generate income from stocks you already hold, and cash-secured puts to potentially buy stocks at a lower price. Match the strategy to your goals and market expectations for the best results.

What are the key risks of using covered calls or cash-secured puts?

When using covered calls, a key risk is that you might be obligated to sell your stock at the strike price if the option is exercised. This could limit your potential gains if the stock’s price rises significantly. On the flip side, if the stock’s value drops, you’ll still face losses on the shares you own. However, the premium earned from selling the call can help offset some of that decline.

For cash-secured puts, the main concern is the possibility of being required to buy the stock at the strike price, even if the stock’s market value has dropped below that level. This means you could end up purchasing the stock at a price higher than its current market value, leading to an immediate unrealized loss. If the stock experiences a sharp decline, the premium you received might not be enough to fully offset the drop.

Both approaches demand a close look at market conditions, the stock’s volatility, and your investment objectives to navigate these risks effectively.