Adjusting Options Positions for Volatility Changes

How implied volatility affects option positions and practical adjustments: hedge or convert positions, roll expirations, sell high IV premium, and manage Delta/Vega/Theta.

Implied volatility (IV) can make or break your options trades. Even if your price prediction is spot on, changes in IV can erode your profits or amplify losses. Here's what you need to know:

- What is IV? It measures market expectations of future price movement. Higher IV means higher option premiums; lower IV means lower premiums.

- Why it matters: A 1% change in IV can shift option premiums by 0.15%–0.35%. IV spikes during uncertainty (e.g., bearish markets) and drops during calm periods or after major events.

- Key risk: IV Crush - a sharp drop in IV after events like earnings can wipe out gains, even when the stock moves in your favor.

Quick Tips for Managing Volatility

- Rising IV: Transition to spreads (e.g., vertical credit spreads) to limit losses from negative Vega exposure.

- Falling IV: Sell options like covered calls when IV is high to benefit from premium shrinkage as IV normalizes.

- Track metrics: Use Delta, Vega, and Theta to time adjustments and manage risk.

Volatility is unpredictable, but understanding how it affects your positions - and adjusting accordingly - can protect your portfolio and improve outcomes.

How Rising and Falling Volatility Affects Your Positions

Volatility changes can significantly impact your positions, introducing risks that vary depending on whether implied volatility (IV) rises or falls. Recognizing these dynamics can help you prepare for potential challenges before they undermine your portfolio. Let’s break down how these issues arise under both rising and falling volatility conditions.

Problems from Rising Volatility

A spike in IV can quickly erode profits for option sellers. For example, when the VIX jumps from 15 to 40, short option positions often lose value rapidly. This happens because short options have negative Vega, meaning they lose money as IV increases.

During volatility surges, the balance between Theta (time decay) and Vega becomes a critical factor. While Theta provides a steady income stream, sudden increases in IV can overwhelm those gains. As Andy Crowder explains:

"While theta provides steady erosion, gamma and vega can rapidly escalate losses".

For strategies like straddles, strangles, and iron condors, this dynamic can result in significant paper losses - even when the strikes remain untouched. Options that are at-the-money or have longer durations are particularly vulnerable. For instance, a 180-day option with a Vega of 0.42 would lose $2.10 per share for every 1% rise in IV, compared to just $0.40 for a 7-day option.

Problems from Falling Volatility

Declining IV, on the other hand, introduces a different set of challenges. When IV drops, premiums shrink, reducing the income potential for option sellers. This is especially problematic for existing long positions, as falling IV leads to value erosion through negative Vega exposure. Even if the underlying stock price remains stable, options lose extrinsic value as IV declines.

The problem becomes more pronounced when IV is at historical lows. Selling premium during these periods can be risky, as the compensation for taking on risk may not be sufficient. Monitoring IV Rank, which compares current IV to its range over the past 52 weeks, can help you avoid entering positions when premiums are too low to justify the strategy.

These scenarios highlight the importance of having precise adjustment strategies, which will be explored in the next sections.

sbb-itb-a9ac3c2

How to Adjust Your Positions When Volatility Changes

When volatility shifts, it’s essential to adapt your strategy to protect your portfolio. Managing Vega exposure and rebalancing your positions to match the new volatility environment are key steps. The adjustments you make will depend on whether volatility is rising or falling. Below, we’ll explore specific strategies for each scenario.

Adjusting for Rising Volatility

During periods of heightened volatility, reducing net negative Vega exposure becomes a priority. One effective way to do this is by converting naked short positions into vertical credit spreads. This involves buying further out-of-the-money options to cap potential losses and reduce sensitivity to Vega.

Another adjustment is rolling your positions to longer expirations. This allows you to capture greater Theta decay as volatility stabilizes. Additionally, you can exploit inefficiencies in the term structure of implied volatility (IV). For example, if front-month IV is significantly higher than back-month IV, long calendar spreads can be profitable. In this strategy, you sell the inflated front-month options and buy back-month options, benefiting as near-term volatility normalizes.

For a more aggressive hedge, consider buying long-dated LEAPS, VIX futures, or VIX call options to counteract negative Vega exposure. A real-world example of extreme volatility occurred during the January 2021 GameStop event, where 90-day options saw IV soar to 322% before dropping to 179% within a month.

While rising volatility requires defensive adjustments to limit losses, falling volatility presents opportunities to capture gains.

Adjusting for Falling Volatility

When volatility begins to decline, the focus shifts to strategies that take advantage of premium contraction. Selling options when IV is high can be a profitable move, as IV often reverts to its mean. As Investopedia explains:

"Option traders typically sell, or write, options when implied volatility is high because this means selling or 'going short' on volatility, betting that it will revert to the mean".

Strategies like short straddles and iron condors are particularly effective in low-volatility environments. These approaches allow you to collect inflated premiums while benefiting from both time decay and falling IV. If IV drops sharply after a volatility event, consider closing positions early to lock in Vega-related gains.

You can also take advantage of volatility skew by selling high-IV out-of-the-money puts following a spike. This is especially effective when put IV remains elevated compared to call IV. Monitoring indicators like the Average Directional Index (ADX) can further guide your strategy. When the ADX falls below 25, it signals a weakening trend - an ideal condition for deploying low-volatility strategies.

Using Roll Strategies and Risk Metrics to Manage Volatility

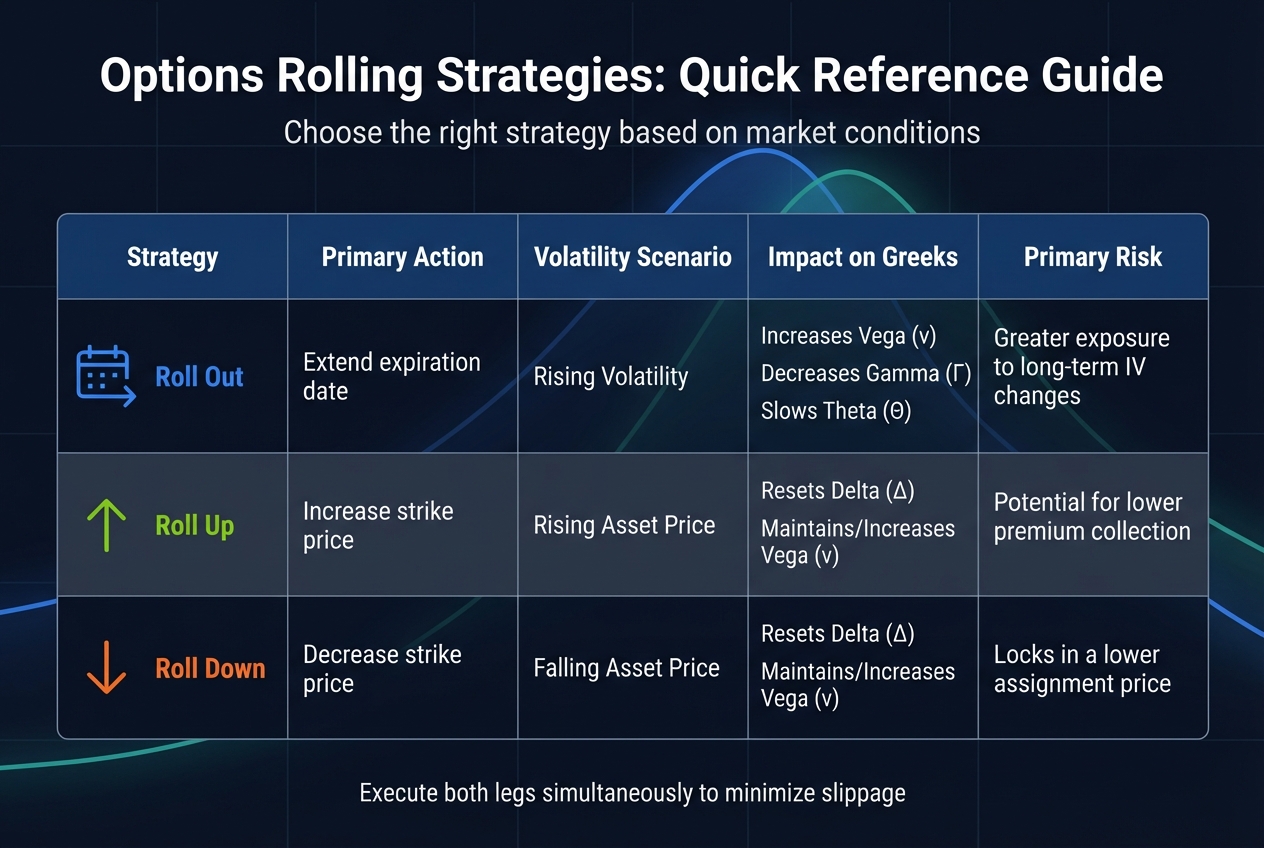

Options Rolling Strategies Comparison: Roll Out vs Roll Up vs Roll Down

Managing volatility effectively in options trading often comes down to using the right roll strategies and understanding key risk metrics. Rolling your options positions allows you to adapt to market changes without closing a trade entirely. By adjusting the strike price, expiration date, or both, you can realign your position with current conditions. The key lies in selecting the appropriate strategy and timing adjustments based on risk metrics.

Comparing Roll Strategies

Each roll strategy serves a specific purpose, depending on how volatility and the underlying asset are behaving. Here's how three main strategies stack up:

| Strategy | Primary Action | Volatility Scenario | Impact on Greeks | Primary Risk |

|---|---|---|---|---|

| Roll Out | Extend expiration date | Rising Volatility | Increases Vega; Decreases Gamma; Slows Theta | Greater exposure to long-term IV changes |

| Roll Up | Increase strike price | Rising Asset Price | Resets Delta; Maintains/Increases Vega | Potential for lower premium collection |

| Roll Down | Decrease strike price | Falling Asset Price | Resets Delta; Maintains/Increases Vega | Locks in a lower assignment price |

- Rolling out is useful when volatility is expected to stay high. It slows time decay (Theta) and increases sensitivity to implied volatility (Vega).

- Rolling up is ideal for locking in gains or avoiding assignment when the stock price rises above your short call strike.

- Rolling down allows you to protect put profits or reposition after a stock price drop.

For example, in October 2025, a trader managing an Advanced Micro Devices (AMD) position showcased a practical application of rolling. After a 60% rally in AMD, the trader sold November $200 calls (initially purchased for $3.80, later valued at $63.55) and bought November $270 calls for $15.25. This roll generated a net credit of $48.30 and secured approximately $44.50 in profit while keeping exposure to further upside gains.

How Risk Metrics Guide Volatility Adjustments

Risk metrics like Delta, Gamma, Vega, and Theta are essential tools for timing and executing roll adjustments. Here's how each metric plays a role:

- Delta reflects the likelihood of an option expiring in-the-money. Traders often roll covered calls when Delta reaches 0.55–0.65, signaling heightened assignment risk.

- Gamma measures how quickly Delta changes. Gamma spikes for at-the-money options as expiration nears, especially in the final week. To avoid this risk, many traders roll their positions 21 days before expiration, sidestepping the "gamma zone".

- Vega shows sensitivity to implied volatility. When volatility spikes (e.g., during a VIX surge), rolling into vertical spreads can help neutralize negative Vega exposure and cap potential losses.

- Theta tracks time decay, which speeds up as expiration approaches. Since the last 25% of an option's life accounts for roughly 50% of total Theta decay, premium sellers often target 30–45 days to expiration to maximize the theta-to-gamma ratio. Another signal to roll is when extrinsic value drops below 10–15% of the option's total price.

"Every options position is fundamentally a bet on whether realized movement (Gamma) will exceed the cost of time (Theta)." - StrikeWatch EA Research Team

When rolling, it's crucial to execute both legs - buy to close and sell to open - at the same time. This minimizes slippage and reduces the chance of adverse market moves during the trade. Always confirm the net credit or debit before rolling; a well-timed roll should either generate a credit or involve a manageable cost that aligns with your risk management goals.

Using ThetaEdge to Make Better Adjustments

How ThetaEdge Simplifies Volatility Management

Managing options during volatile markets can feel like trying to solve a puzzle where the pieces keep shifting. ThetaEdge steps in to streamline this process, offering real-time insights and automation to help traders adapt quickly. Its AI-powered agent, Thetix, analyzes your portfolio alongside live market data, cutting through the complexity and reducing the risk of errors.

The platform's dynamic dashboards provide real-time updates, so you can monitor volatility changes and portfolio risks without tedious recalculations. When market conditions shift - like a spike or dip in implied volatility - Thetix highlights what’s changed, explains why, and lays out the trade-offs for potential adjustments. You can even ask questions in plain English, such as, "What happens to my Vega exposure if I roll this covered call?" Thetix responds with clear, actionable insights, helping you make informed decisions without the guesswork.

"Finally usable options data means I don't second-guess my covered calls. I just see the reasoning and make the move." - Daniel Harper, Biotech Research Lead

This level of clarity and immediacy makes it easier to stay on top of volatility, even in fast-moving markets.

Features That Support Volatility Adjustments

ThetaEdge doesn’t just analyze data - it equips you with tools to act on it. The platform includes customizable alerts and dashboards tailored to your trading needs. For example, Thetix Alerts allow you to set conditions like "alert me when implied volatility exceeds 40%" or "when Delta reaches 0.60." These alerts ensure you’re notified the moment your positions require attention, leveraging key metrics like Delta and Vega to keep you ahead of the curve.

Daily Thetix Reports provide a summary of action items and expiration alerts, sent straight to your inbox. These reports highlight which positions might need rolling or other adjustments based on the latest market conditions. For a broader view, you can organize analytical cards into a personalized Risk Center dashboard, giving you a snapshot of how changes in implied volatility impact your overall portfolio.

ThetaEdge also integrates seamlessly with your existing brokerage account using secure, read-only access. While the platform provides the analysis and adjustment strategies, you maintain full control over executing trades through your preferred broker. For those curious to explore its capabilities, a free trial with full feature access is available.

"I stopped guessing. Thetix shows me the numbers and the context so I can trade with confidence." - Sophia Martinez, Operations Manager

Conclusion

Key Takeaways

Volatility can either erode or enhance your trading positions. Vega, which measures an option's sensitivity to a 1% change in implied volatility, plays a crucial role here. When the VIX surges by 20% to 50% in a single day, unmanaged negative Vega can lead to rapid losses.

Rising volatility inflates option premiums, creating immediate mark-to-market losses for premium sellers. On the other hand, a drop in volatility - often seen after earnings announcements - can cause an "IV crush", draining option value even if the stock moves in your favor. To navigate these shifts, it's essential to adjust your positions dynamically. This might involve converting naked positions into defined-risk spreads during VIX spikes, rolling positions further out when implied volatility is elevated, or using VIX-related hedges to counter systemic risk.

"Vega risk is the primary reason why otherwise successful options strategies can fail spectacularly during low-probability, high-impact market events." - QuantStrategy.io Team

Keeping an eye on IV Rank vs IV Percentile - which compares current implied volatility to its 52-week range - can help you capitalize on expensive premiums and benefit as volatility reverts to the mean. Tools like ThetaEdge make this process easier by tracking your Net Vega exposure, sending real-time alerts when volatility thresholds are crossed, and offering AI-driven insights through Thetix to guide your adjustments effectively.

FAQs

How can I tell if my position is too exposed to Vega?

To understand your Vega exposure, you need to measure how much your options position reacts to changes in implied volatility. A higher Vega indicates that your position is more sensitive to these shifts, which can directly affect your profits or losses. Start by calculating your Vega and weighing it against your risk tolerance or the size of your portfolio. If the exposure seems too large, you might want to adjust by hedging or scaling back Vega exposure. This approach can help you manage risk, especially in periods of heightened market volatility.

When should I roll instead of closing the trade?

Sometimes, instead of closing an options position, you might choose to roll it. This approach is ideal when you want to extend the trade's duration, adjust the strike price or expiration date, or respond to shifts in market conditions. Rolling can help you maintain the potential for gains, manage risk, or sidestep assignment as expiration nears - especially if the trade still matches your market expectations.

How can I avoid an IV crush around earnings?

When navigating earnings season, avoiding an IV crush is all about timing and strategy. One approach is to trade before implied volatility reaches its peak, allowing you to benefit from the natural rise in volatility leading up to the earnings announcement. Another tactic is to time your trades carefully, aiming to capitalize on the volatility spike while minimizing your exposure to the subsequent drop. Alternatively, you can structure your positions in a way that reduces the impact of the post-earnings volatility drop, helping to shield your portfolio from sudden value declines. These strategies can help you manage the risks associated with earnings-related volatility adjustments.